AI and Data Analysis in Livestock

The Quantitative Finance and AI Outlook

Factor models are widely used in quantitative finance to decompose asset returns into systematic risk components. In the context of Environmental, Social, and Governance (ESG) investing, factor models help assess how ESG factors influence portfolio performance, risk, and diversification. By incorporating ESG-related factors into traditional factor models, investors can quantify ESG impact on portfolio risk-adjusted returns.

Quantitative Sustainable and ESG (Environmental, Social, and Governance) Portfolio Construction is an advanced investment framework that integrates sustainability considerations into systematic portfolio management. This approach combines quantitative finance techniques with ESG metrics to enhance risk-adjusted returns while aligning investments with ethical, environmental, and social objectives.

The Quantitative Trading Workshop is an educational event focused on algorithmic trading strategies, statistical methods, and financial data analysis. It covers topics such as market dynamics, risk management, machine learning in trading, and backtesting strategies. Participants gain hands-on experience with coding (Python/R) and quantitative models, making it ideal for finance professionals, researchers, and students interested in systematic trading.

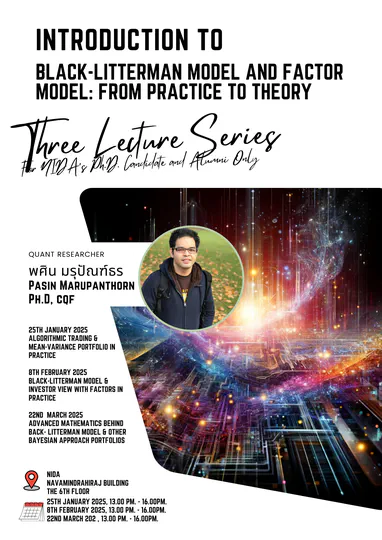

This lecture series provides a comprehensive journey from practical applications to theoretical foundations of the Black-Litterman Model and Factor Model in portfolio management. The sessions will explore algorithmic trading, Bayesian approaches, and the integration of investor views with factors in portfolio construction.

The session will explore strategies for pair trading across multiple assets, focusing on identifying pairs, statistical arbitrage, and risk management techniques. Practical applications, mathematical modeling, and real-world case studies will be discussed to enhance understanding of quantitative strategies for multi-asset trading.

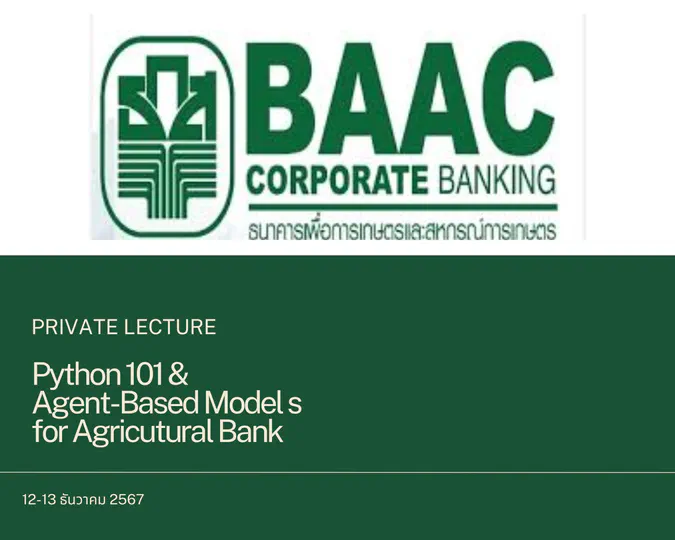

This lecture will introduce Python programming fundamentals and their application in developing Agent-Based Models (ABM). Topics include Python basics, simulation design, and modeling individual agents to understand complex systems such as markets, ecosystems, and social behaviors. Practical examples and hands-on exercises will be provided.

This study evaluates the impact of ESG (Environmental, Social, and Governance) sustainability factors on U.S. equity indices using various factor models. The analysis focuses on Morningstar's U.S. market and sustainability indices from 2013 to 2022, excluding the COVID-19 period. The study employs three types of models, a standard factor model, a time series factor model, and a functional factor model. The standard factor model assesses the instantaneous effect of ESG factors on index returns, revealing that sustainability indices effectively mitigate ESG-related risks, while traditional U.S. indices are more sensitive to these factors. The time series factor model investigates the time-lagging effects of ESG factors, showing that sustainability indices exhibit a stronger correlation with ESG factors over time, especially in the short term. Finally, the functional factor model explores the dynamic and cumulative effects of ESG factors, highlighting their significant impact on sustainability indices compared to traditional indices.

The event provided an overview of the M.Sc. Financial Engineering program at WorldQuant University, highlighting its tuition-free, globally recognized curriculum that combines theoretical and practical aspects of quantitative finance. Key discussions covered the program structure, application process, and career opportunities in fields like algorithmic trading and risk management. Alumni and students shared their experiences, emphasizing the program's flexibility and real-world relevance. A Q&A session addressed attendees' queries, showcasing how the program equips graduates for successful careers in finance. The event underscored the accessibility and value of the program for aspiring financial engineers.

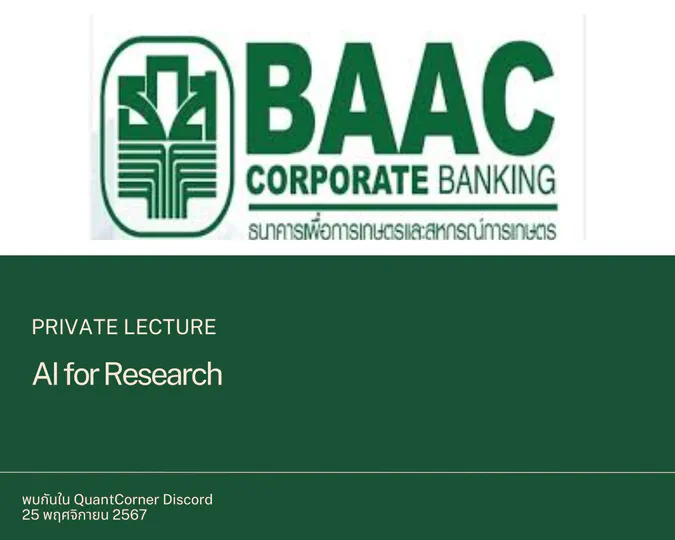

This lecture will explore the applications of Artificial Intelligence (AI) in research, focusing on how machine learning, data analytics, and AI tools can enhance research methodologies. Practical case studies and examples will demonstrate AI's role in improving decision-making, data processing, and innovation across various research fields.

This lecture will provide an introduction to quantitative trading, covering key concepts such as algorithmic strategies, data-driven decision-making, backtesting, and risk management. Participants will gain insights into how quantitative techniques are applied to develop trading systems and optimize performance in modern financial markets.

The Certificate in Quantitative Finance (CQF) offers information sessions designed to provide insights into the program's structure, curriculum, and benefits. These sessions are ideal for professionals aiming to advance their careers in quantitative finance.

Quantitative careers, commonly referred to as "Quant Careers," involve roles where professionals apply mathematical, statistical, and computational methods to solve problems in finance, insurance, technology, and other industries. Here’s a structured guideline to help you navigate and succeed in a quant career.

Lecturer on AI tools that enhance productivity for researchers

The event provided undergraduate students with practical advice on selecting, planning, and executing research projects in financial mathematics. It covered key areas such as choosing relevant topics, applying mathematical models and computational techniques, structuring projects, and connecting theoretical concepts to real-world financial problems. Additionally, students received guidance on effective communication of research findings and participated in a Q&A session to address individual queries. The event aimed to equip students with the skills and confidence needed to excel in their academic projects and bridge the gap between theory and practice.

Discussion on King Quant Trading Strategy, Jim Simons Biography, and Guideline for Money Formula

Providing a structured framework to effectively plan, execute, and present mathematical research and applications.

The qunatitaive trading

An example talk using Hugo Blox Builder's Markdown slides feature.

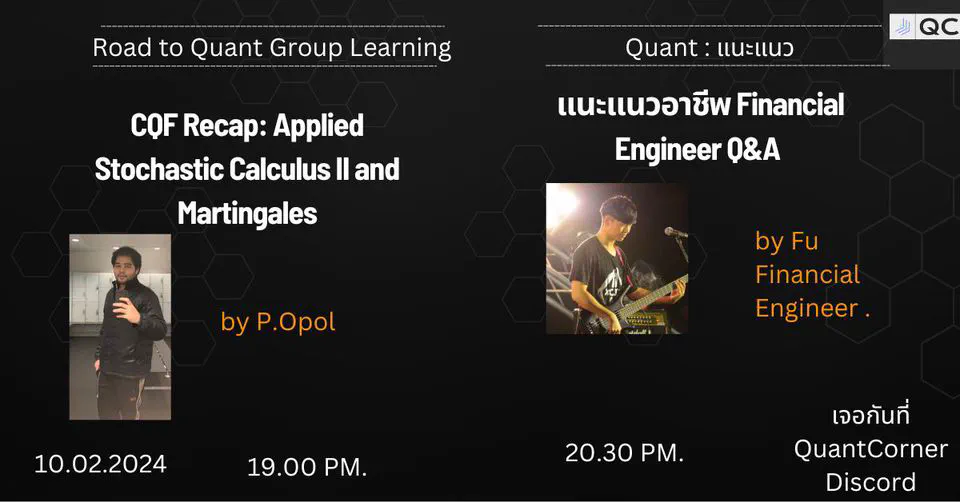

The CQF Recap provides a comprehensive review of key concepts, while Applied Stochastic Calculus II delves into advanced stochastic processes, and the study of Martingales focuses on their properties and applications in financial mathematics.

To succeed at WorldQuant University, familiarize yourself with the curriculum and course materials, and manage your time effectively by creating and adhering to a study schedule.

Developing divestment strategies is essential for carbon reduction.

Investing in option market microstructure involves understanding the detailed mechanisms of order execution, price formation, and liquidity provision in option markets to optimize trading strategies and manage risks effectively.

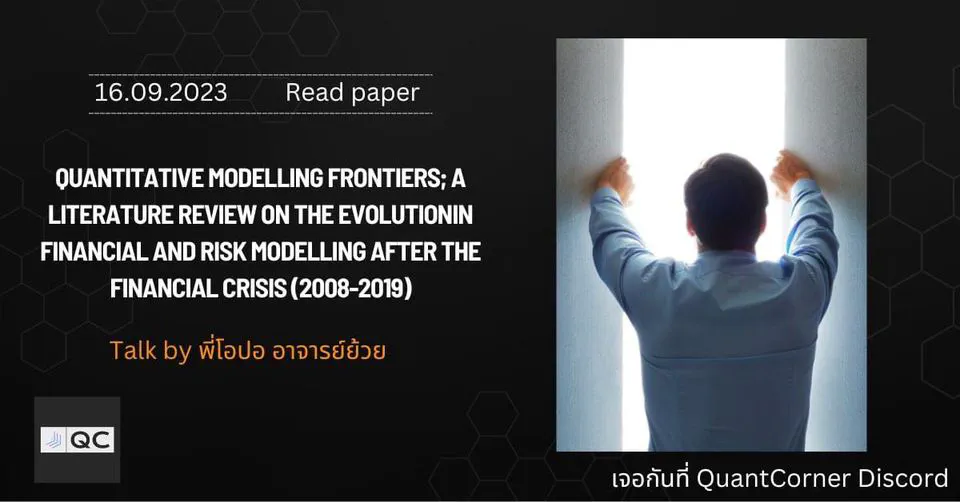

Examines the advancements and changes in financial and risk modelling practices in response to the financial crisis, highlighting significant developments and trends in the field over the specified period.

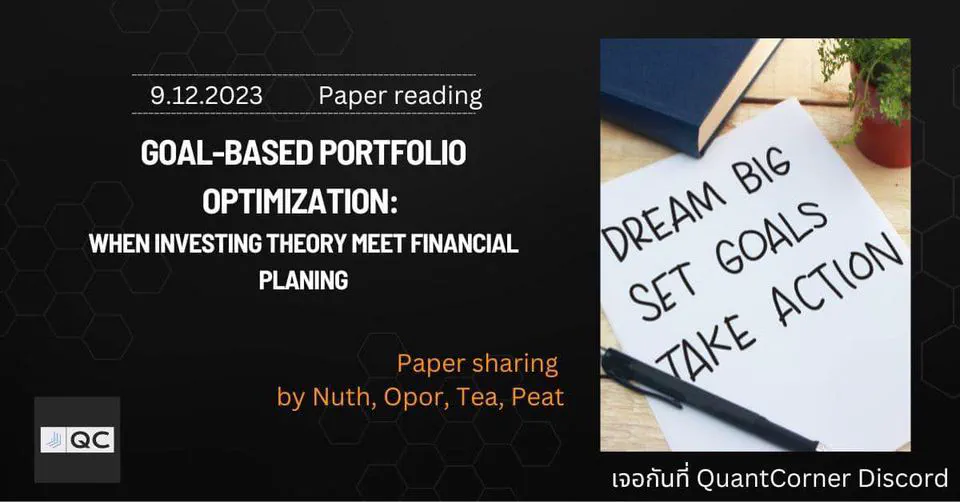

Goal-based portfolio optimization is a strategy that tailors investment decisions to meet specific financial objectives by aligning asset allocation and risk management with the investor's individual goals and time horizons.

Exploring introductory econophysics models and the relationship between financial and physical systems

Semimar on the modern actuarial mathematics . including the sustainable insurance, decentralized insurance and machine learning in insurance

Seminar on portfolio optimization with limiting the carbon footprint