Asymptotic Confidence Ellipse for Lognormal Distribution with Applications in Actuarial Pricing

Jan 19, 2025·, ·

0 min read

·

0 min read

Nassamon Bootwisas

Uparittha Intarasat

Pasin Marupanthorn

Image credit:

Image credit:Abstract

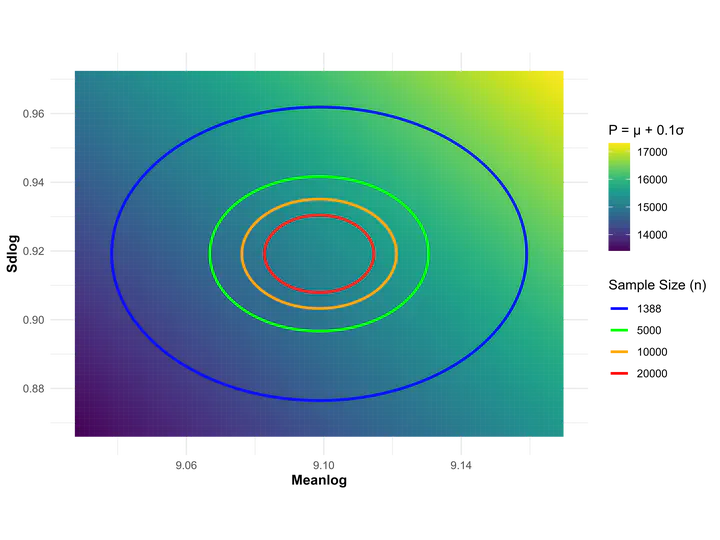

This paper presents the construction and validation of asymptotic confidence ellipses for the parameters of the lognormal distribution, leveraging the asymptotic properties of Maximum Likelihood Estimators (MLEs). Using Monte Carlo simulations across various parameter settings, the study evaluates the performance of these asymptotic confidence ellipses. The results demonstrate that the ellipses provide accurate parameter estimates and coverage probabilities that closely align with the nominal confidence level of 95%, with coverage ranging from 94.27% to 95.13%, even for small sample sizes. The lower bound of the sample size required to achieve a given level of accuracy is derived based on the asymptotic confidence ellipse of the lognormal distribution and validated through simulations. An application to health insurance pricing demonstrates the use of the asymptotic confidence ellipse to visualize uncertainty in parameter estimators and premiums under the lognormal loss distribution. It also facilitates deriving confidence intervals for premiums and determining the required policy sales to achieve desired pricing accuracy.

Type